Chapter 4: Linear models#

Concept map:

Notebook setup#

import numpy as np

import pandas as pd

import scipy as sp

import seaborn as sns

from scipy.stats import uniform, norm

# notebooks figs setup

%matplotlib inline

import matplotlib.pyplot as plt

sns.set(rc={'figure.figsize':(8,5)})

blue, orange = sns.color_palette()[0], sns.color_palette()[1]

# silence annoying warnings

import warnings

warnings.filterwarnings('ignore')

4.1 Linear models for relationship between two numeric variables#

def’n linear model: y ~ m*x + b, a.k.a. linear regression

Amy has collected a new dataset:

Instead of receiving a fixed amount of stats training (100 hours), each employee now receives a variable amount of stats training (anywhere from 0 hours to 100 hours)

Amy has collected ELV values after one year as previously

Goal find best fit line for relationship \(\textrm{ELV} \sim \beta_0 + \beta_1\!*\!\textrm{hours}\)

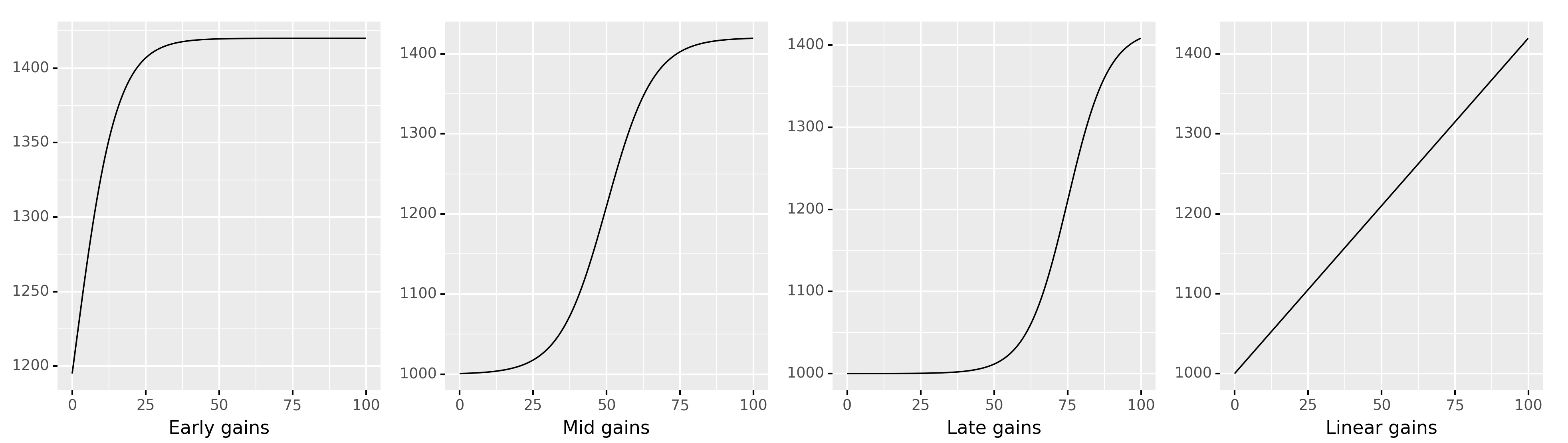

Limitation: we assume the change in ELV is proportional to number of hours (i.e. linear relationship). Other types of hours-ELV relationship possible, but we will not be able to model them correctly (see figure below).

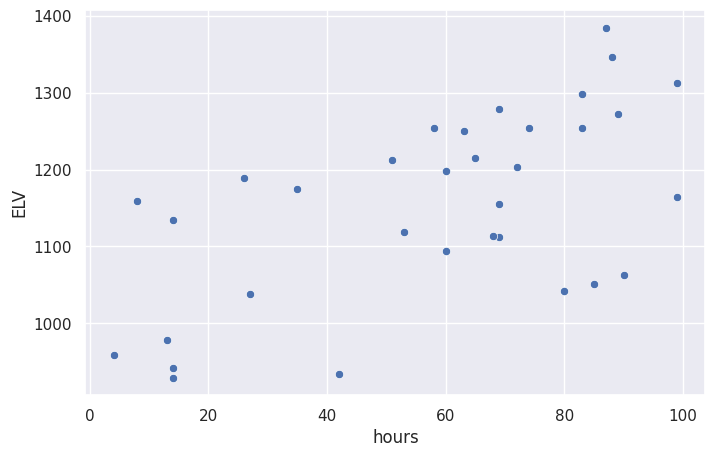

New dataset#

The

hourscolumn contains thexvalues (how many hours of statistics training did the employee receive),The

ELVcolumn contains theyvalues (the employee ELV after one year)

# Load data into a pandas dataframe

df2 = pd.read_excel("data/ELV_vs_hours.ods", sheet_name="Data")

# df2

df2.describe()

| hours | ELV | |

|---|---|---|

| count | 33.000000 | 33.000000 |

| mean | 57.909091 | 1154.046364 |

| std | 28.853470 | 123.055405 |

| min | 4.000000 | 929.200000 |

| 25% | 35.000000 | 1062.210000 |

| 50% | 65.000000 | 1163.890000 |

| 75% | 83.000000 | 1253.620000 |

| max | 99.000000 | 1384.480000 |

# plot ELV vs. hours data

sns.scatterplot(x='hours', y='ELV', data=df2)

<Axes: xlabel='hours', ylabel='ELV'>

# linear model plot (preview)

# sns.lmplot(x='hours', y='ELV', data=df2, ci=False)

Types of linear relationship between input and output#

Different possible relationships between the number of hours of stats training and ELV gains:

4.2 Fitting linear models#

Main idea: use

fitmethod fromstatsmodels.olsand a formula (approach 1)Visual inspection

Results of linear model fit are:

beta0= \(\beta_0\) = baseline ELV (y-intercept)beta1= \(\beta_1\) = increase in ELV for each additional hour of stats training (slope)

Five more alternative fitting methods (bonus material): 2. fit using statsmodels

OLS3. solution usinglinregressfromscipy4. solution usingoptimizefromscipy5. linear algebra solution usingnumpy6. solution usingLinearRegressionmodel from scikit-learn

Using statsmodels formula API#

The statsmodels Python library offers a convenient way to specify statistics model as a “formula” that describes the relationship we’re looking for.

Mathematically, the linear model is written:

\(\large \textrm{ELV} \ \ \sim \ \ \beta_0\cdot 1 \ + \ \beta_1\cdot\textrm{hours}\)

and the formula is:

ELV ~ 1 + hours

Note the variables \(\beta_0\) and \(\beta_1\) are omitted, since the whole point of fitting a linear model is to find these coefficients. The parameters of the model are:

Instead of \(\beta_0\), the constant parameter will be called

InterceptInstead of a new name \(\beta_1\), we’ll call it

hourscoefficient (i.e. the coefficient associated with thehoursvariable in the model)

import statsmodels.formula.api as smf

model = smf.ols('ELV ~ 1 + hours', data=df2)

result = model.fit()

# extact the best-fit model parameters

beta0, beta1 = result.params

beta0, beta1

(1005.6736305656403, 2.562166505145919)

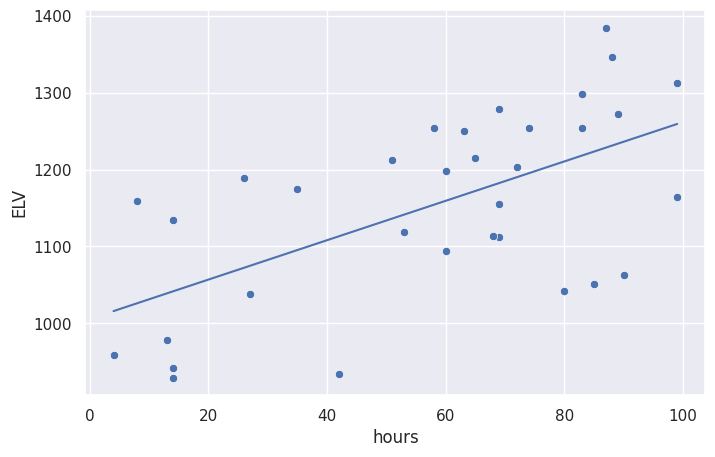

# data points

sns.scatterplot(x='hours', y='ELV', data=df2)

# linear model for data

x = df2['hours'].values # input = hours

ymodel = beta0 + beta1*x # output = ELV

sns.lineplot(x=x, y=ymodel)

<Axes: xlabel='hours', ylabel='ELV'>

result.summary()

| Dep. Variable: | ELV | R-squared: | 0.361 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.340 |

| Method: | Least Squares | F-statistic: | 17.51 |

| Date: | Fri, 17 Jul 2026 | Prob (F-statistic): | 0.000218 |

| Time: | 16:57:27 | Log-Likelihood: | -197.75 |

| No. Observations: | 33 | AIC: | 399.5 |

| Df Residuals: | 31 | BIC: | 402.5 |

| Df Model: | 1 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| Intercept | 1005.6736 | 39.499 | 25.461 | 0.000 | 925.115 | 1086.232 |

| hours | 2.5622 | 0.612 | 4.184 | 0.000 | 1.313 | 3.811 |

| Omnibus: | 4.012 | Durbin-Watson: | 2.135 |

|---|---|---|---|

| Prob(Omnibus): | 0.135 | Jarque-Bera (JB): | 2.166 |

| Skew: | -0.368 | Prob(JB): | 0.339 |

| Kurtosis: | 1.983 | Cond. No. | 146. |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Alternative model fitting methods#

fit using statsmodels

OLSsolution using

linregressfromscipysolution using

minimizefromscipylinear algebra solution using

numpysolution using

LinearRegressionmodel from scikit-learn

Data pre-processing#

The statsmodels formula ols approach we used above was able to get the data

directly from the dataframe df2, but some of the other model fitting methods

require data to be provided as regular arrays: the x-values and the y-values.

# extract hours and ELV data from df2

x = df2['hours'].values # hours data as an array

y = df2['ELV'].values # ELV data as an array

x.shape, y.shape

# x

((33,), (33,))

Two of the approaches required “packaging” the x-values along with a column of ones,

to form a matrix (called a design matrix). Luckily statsmodels provides a convenient function for this:

import statsmodels.api as sm

# add a column of ones to the x data

X = sm.add_constant(x)

X.shape

# X

(33, 2)

2. fit using statsmodels OLS#

model2 = sm.OLS(y, X)

result2 = model2.fit()

# result2.summary()

result2.params

array([1005.67363057, 2.56216651])

3. solution using linregress from scipy#

from scipy.stats import linregress

result3 = linregress(x, y)

result3.intercept, result3.slope

(np.float64(1005.6736305656411), np.float64(2.562166505145915))

4. Using an optimization approach#

from scipy.optimize import minimize

def sse(beta, x=x, y=y):

"""Compute the sum-of-squared-errors objective function."""

sumse = 0.0

for xi, yi in zip(x, y):

yi_pred = beta[0] + beta[1]*xi

ei = (yi_pred-yi)**2

sumse += ei

return sumse

result4 = minimize(sse, x0=[0,0])

beta0, beta1 = result4.x

beta0, beta1

(np.float64(1005.6733420314862), np.float64(2.5621705087641646))

5. Linear algebra solution#

We obtain the least squares solution using the Moore–Penrose inverse formula: $\( \large \vec{\beta} = (X^{\sf T} X)^{-1}X^{\sf T}\; \vec{y} \)$

# 5. linear algebra solution using `numpy`

import numpy as np

result5 = np.linalg.inv(X.T.dot(X)).dot(X.T).dot(y)

beta0, beta1 = result5

beta0, beta1

(np.float64(1005.6736305656412), np.float64(2.562166505145917))

Using scikit-learn#

# 6. solution using `LinearRegression` from scikit-learn

# %pip install scikit-learn

# from sklearn import linear_model

# model6 = linear_model.LinearRegression()

# model6.fit(x[:,np.newaxis], y)

# model6.intercept_, model6.coef_

# (1005.673630565641, array([2.56216651]))

4.3 Interpreting linear models#

model fit checks

\(R^2\) coefficient of determination = the proportion of the variation in the dependent variable that is predictable from the independent variable

plot of residuals

many other: see scikit docs

hypothesis tests

is slope zero or nonzero? (and CI interval)

caution: cannot make any cause-and-effect claims; only a correlation

Predictions

given best-fir model obtained from data, we can make predictions (interpolations),

e.g., what is the expected ELV after 50 hours of stats training?

Interpreting the results#

Let’s review some of the other data included in the results.summary() report for the linear model fit we did earlier.

result.summary()

| Dep. Variable: | ELV | R-squared: | 0.361 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.340 |

| Method: | Least Squares | F-statistic: | 17.51 |

| Date: | Fri, 17 Jul 2026 | Prob (F-statistic): | 0.000218 |

| Time: | 16:57:28 | Log-Likelihood: | -197.75 |

| No. Observations: | 33 | AIC: | 399.5 |

| Df Residuals: | 31 | BIC: | 402.5 |

| Df Model: | 1 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| Intercept | 1005.6736 | 39.499 | 25.461 | 0.000 | 925.115 | 1086.232 |

| hours | 2.5622 | 0.612 | 4.184 | 0.000 | 1.313 | 3.811 |

| Omnibus: | 4.012 | Durbin-Watson: | 2.135 |

|---|---|---|---|

| Prob(Omnibus): | 0.135 | Jarque-Bera (JB): | 2.166 |

| Skew: | -0.368 | Prob(JB): | 0.339 |

| Kurtosis: | 1.983 | Cond. No. | 146. |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Model parameters#

beta0, beta1 = result.params

result.params

Intercept 1005.673631

hours 2.562167

dtype: float64

The \(R^2\) coefficient of determination#

\(R^2 = 1\) corresponds to perfect prediction

result.rsquared

np.float64(0.36091871798872777)

Hypothesis testing for slope coefficient#

Is there a non-zero slope coefficient?

null hypothesis \(H_0\):

hourshas no effect onELV, which is equivalent to \(\beta_1 = 0\): $\( \large H_0: \qquad \textrm{ELV} \sim \mathcal{N}(\color{red}{\beta_0}, \sigma^2) \qquad \qquad \qquad \)$alternative hypothesis \(H_A\):

hourshas an effect onELV, and the slope is not zero, \(\beta_1 \neq 0\): $\( \large H_A: \qquad \textrm{ELV} \sim \mathcal{N}\left( \color{blue}{\beta_0 + \beta_1\!\cdot\!\textrm{hours}}, \ \sigma^2 \right) \)$

# p-value under the null hypotheis of zero slope or "no effect of `hours` on `ELV`"

result.pvalues.loc['hours']

np.float64(0.0002184037805991302)

# 95% confidence interval for the hours-slope parameter

# result.conf_int()

CI_hours = list(result.conf_int().loc['hours'])

CI_hours

[1.3132700834428848, 3.811062926848953]

Predictions using the model#

We can use the model we obtained to predict (interpolate) the ELV for future employees.

sns.scatterplot(x='hours', y='ELV', data=df2)

ymodel = beta0 + beta1*x

sns.lineplot(x=x, y=ymodel)

<Axes: xlabel='hours', ylabel='ELV'>

What ELV can we expect from a new employee that takes 50 hours of stats training?

result.predict({'hours':[50]})

0 1133.781956

dtype: float64

result.predict({'hours':[100]})

0 1261.890281

dtype: float64

WARNING: it’s not OK to extrapolate the validity of the model outside of the range of values where we have observed data.

For example, there is no reason to believe in the model’s predictions about ELV for 200 or 2000 hours of stats training:

result.predict({'hours':[200]})

0 1518.106932

dtype: float64

Discussion#

Further topics that will be covered in the book:

Generalized linear models, e.g., Logistic regression

Everything is a linear model article

The verbs

fitandpredictwill come up A LOT in machine learning,

so it’s worth learning linear models in detail to be prepared for further studies.

Congratulations on completing this overview of statistics! We covered a lot of topics and core ideas from the book. I know some parts seemed kind of complicated at first, but if you think about them a little you’ll see there is nothing too difficult to learn. The good news is that the examples in these notebooks contain all the core ideas, and you won’t be exposed to anything more complicated that what you saw here!

If you were able to handle these notebooks, you’ll be able to handle the No Bullshit Guide to Statistics too! In fact the book will cover the topics in a much smoother way, and with better explanations. You’ll have a lot of exercises and problems to help you practice statistical analysis.

Next steps#

I encourage you to check out the book outline shared gdoc if you haven’t seen it already. Please leave me a comment in the google document if you see something you don’t like in the outline, or if you think some important statistics topics are missing. You can also read the book proposal blog post for more info about the book.

Check out also the concept map. You can print it out and annotate with the concepts you heard about in these notebooks.

If you want to be involved in the stats book in the coming months, sign up to the stats reviewers mailing list to receive chapter drafts as they are being prepared (Nov+Dec 2021). I’ll appreciate your feedback on the text. The goal is to have the book finished in the Spring 2022, and feedback and “user testing” will be very helpful.