Section 5.4 — Bayesian difference between means#

This notebook contains the code examples from Section 5.4 Bayesian difference between means from the No Bullshit Guide to Statistics.

See also:

compare_iqs2_many_ways.ipynb

Examples: treszkai/best

Notebook setup#

# Ensure required Python modules are installed

%pip install --quiet numpy scipy seaborn statsmodels bambi==0.15.0 pymc==5.23.0 ministats

[notice] A new release of pip is available: 26.2 -> 26.2.1

[notice] To update, run: pip install --upgrade pip

Note: you may need to restart the kernel to use updated packages.

# Load Python modules

import os

import numpy as np

import pandas as pd

import seaborn as sns

import matplotlib.pyplot as plt

import bambi as bmb

import arviz as az

# Figures setup

plt.clf() # needed otherwise `sns.set_theme` doesn't work

sns.set_theme(

context="paper",

style="whitegrid",

palette="colorblind",

rc={"font.family": "serif",

"font.serif": ["Palatino", "DejaVu Serif", "serif"],

"figure.figsize": (5,3)},

)

%config InlineBackend.figure_format = "retina"

<Figure size 640x480 with 0 Axes>

# Simple float __repr__

if int(np.__version__.split(".")[0]) >= 2:

np.set_printoptions(legacy='1.25')

# Download datasets/ directory if necessary

from ministats import ensure_datasets

ensure_datasets()

datasets/ directory already exists.

Introduciton#

We’ll now revisit the problem of comparison between two groups from a Bayesian perspective.

Model#

The data models for the two groups are based on Student’s \(t\)-distribution:

We’ll use a normal prior for the means, half-\(t\) priors for standard deviations, and a gamma distribution for the degrees of freedom parameter:

Bambi formula objects#

import bambi as bmb

formula = bmb.Formula("y ~ 0 + group",

"sigma ~ 0 + group")

formula

Formula('y ~ 0 + group', 'sigma ~ 0 + group')

formula.main, formula.additionals

('y ~ 0 + group', ('sigma ~ 0 + group',))

formula.get_all_formulas()

['y ~ 0 + group', 'sigma ~ 0 + group']

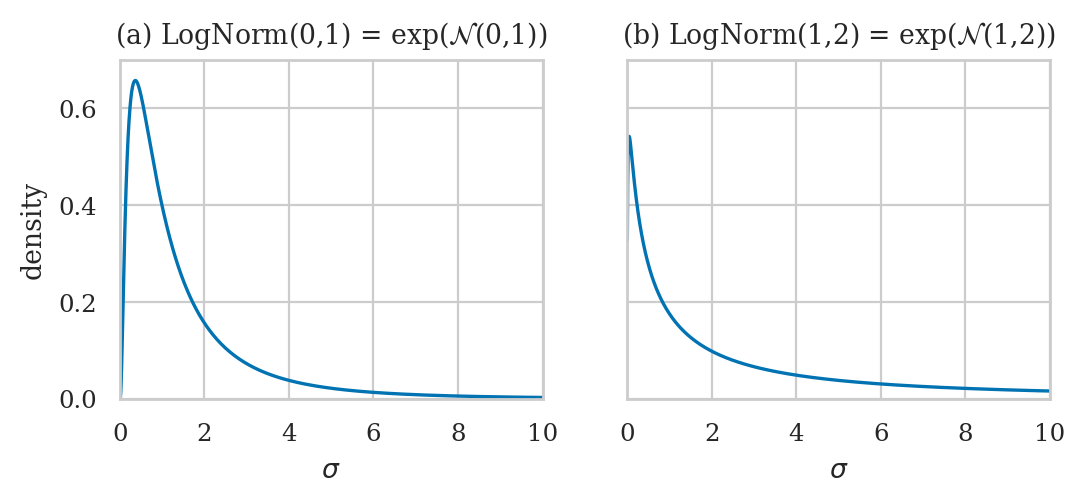

Choosing priors for log-sigma#

Normal distribution for log-sigma#

from scipy.stats import norm

def get_lognormal(mu=0, sigma=1):

logsigs = np.linspace(-5, 5, 1000)

dlogsigs = norm(mu, sigma).pdf(logsigs)

sigmas = np.exp(logsigs)

# Apply the change of variables to get the density for sigma

# based on the Jacobian |d(log(sigma))/d(sigma)| = 1/sigma

dsigmas = dlogsigs / sigmas

return sigmas, dsigmas

with plt.rc_context({"figure.figsize":(6,2.2)}):

fig, (ax1, ax2) = plt.subplots(1,2, sharey=True)

# PLOT 1

mu, sigma = 0, 1

sigmas, dsigmas = get_lognormal(mu, sigma)

sns.lineplot(x=sigmas, y=dsigmas, ax=ax1)

ax1.set_xlabel('$\\sigma$')

ax1.set_ylabel('density')

ax1.set_title(f'(a) LogNorm({mu},{sigma}) = exp($\\mathcal{{N}}$({mu},{sigma}))')

ax1.set_xlim(0, 10)

ax1.set_ylim(0, 0.7)

# PLOT 2

mu, sigma = 1, 2

sigmas, dsigmas = get_lognormal(mu, sigma)

sns.lineplot(x=sigmas, y=dsigmas, ax=ax2)

ax2.set_xlabel('$\\sigma$')

ax2.set_ylabel('density')

ax2.set_title(f'(b) LogNorm({mu},{sigma}) = exp($\\mathcal{{N}}$({mu},{sigma}))')

ax2.set_xlim(0, 10)

Choosing priors for the degrees of freedom parameter#

# FIGURES ONLY

from scipy.stats import gamma as gammadist

from scipy.stats import expon

from ministats import plot_pdf

with plt.rc_context({"figure.figsize":(6,2.2)}):

fig, (ax1, ax2) = plt.subplots(1,2, sharey=True)

# PLOT 1

alpha, beta = 2, 0.1

rv_nu = gammadist(a=2, scale=1/beta)

plot_pdf(rv_nu, rv_name="ν", ax=ax1)

ax1.set_title(f'(a) Gamma($\\alpha=${alpha}, $\\beta=${beta})')

ax1.set_xlim(0, 100)

# PLOT 2

scale = 30

rv_nu_exp = expon(scale=scale)

plot_pdf(rv_nu_exp, rv_name="ν", ax=ax2)

ax2.set_title(f'(b) Expon($\\lambda=$1/{scale})')

ax2.set_xlim(0, 100)

Example 1: comparing electricity prices#

Electricity prices from East End and West End

Electricity prices dataset#

eprices = pd.read_csv("datasets/eprices.csv")

eprices.groupby("loc")["price"].describe()

| count | mean | std | min | 25% | 50% | 75% | max | |

|---|---|---|---|---|---|---|---|---|

| loc | ||||||||

| East | 9.0 | 6.155556 | 0.877655 | 4.8 | 5.5 | 6.3 | 6.5 | 7.7 |

| West | 9.0 | 9.155556 | 1.562139 | 6.8 | 8.3 | 8.6 | 10.0 | 11.8 |

eprices["price"].mean(), eprices["price"].std()

(7.655555555555556, 1.973120020267162)

Bayesian model#

Bambi model#

formula1 = bmb.Formula("price ~ 0 + loc",

"sigma ~ 0 + loc")

links1 = {"mu":"identity",

"sigma":"log"}

priors1 = {

"loc": bmb.Prior("Normal", mu=8, sigma=5),

"sigma": {

"loc": bmb.Prior("Normal", mu=0, sigma=1)

},

"nu": bmb.Prior("Gamma", alpha=2, beta=0.1),

}

mod1 = bmb.Model(formula=formula1,

family="t",

link=links1,

priors=priors1,

data=eprices)

mod1

Formula: price ~ 0 + loc

sigma ~ 0 + loc

Family: t

Link: mu = identity

sigma = log

Observations: 18

Priors:

target = mu

Common-level effects

loc ~ Normal(mu: 8.0, sigma: 5.0)

Auxiliary parameters

nu ~ Gamma(alpha: 2.0, beta: 0.1)

target = sigma

Common-level effects

sigma_loc ~ Normal(mu: 0.0, sigma: 1.0)

mod1.build()

mod1.graph()

Prior predictive checks#

# TODO

Model fitting and analysis#

idata1 = mod1.fit(random_seed=42)

Initializing NUTS using jitter+adapt_diag...

Multiprocess sampling (2 chains in 2 jobs)

NUTS: [nu, loc, sigma_loc]

Sampling 2 chains for 1_000 tune and 1_000 draw iterations (2_000 + 2_000 draws total) took 2 seconds.

We recommend running at least 4 chains for robust computation of convergence diagnostics

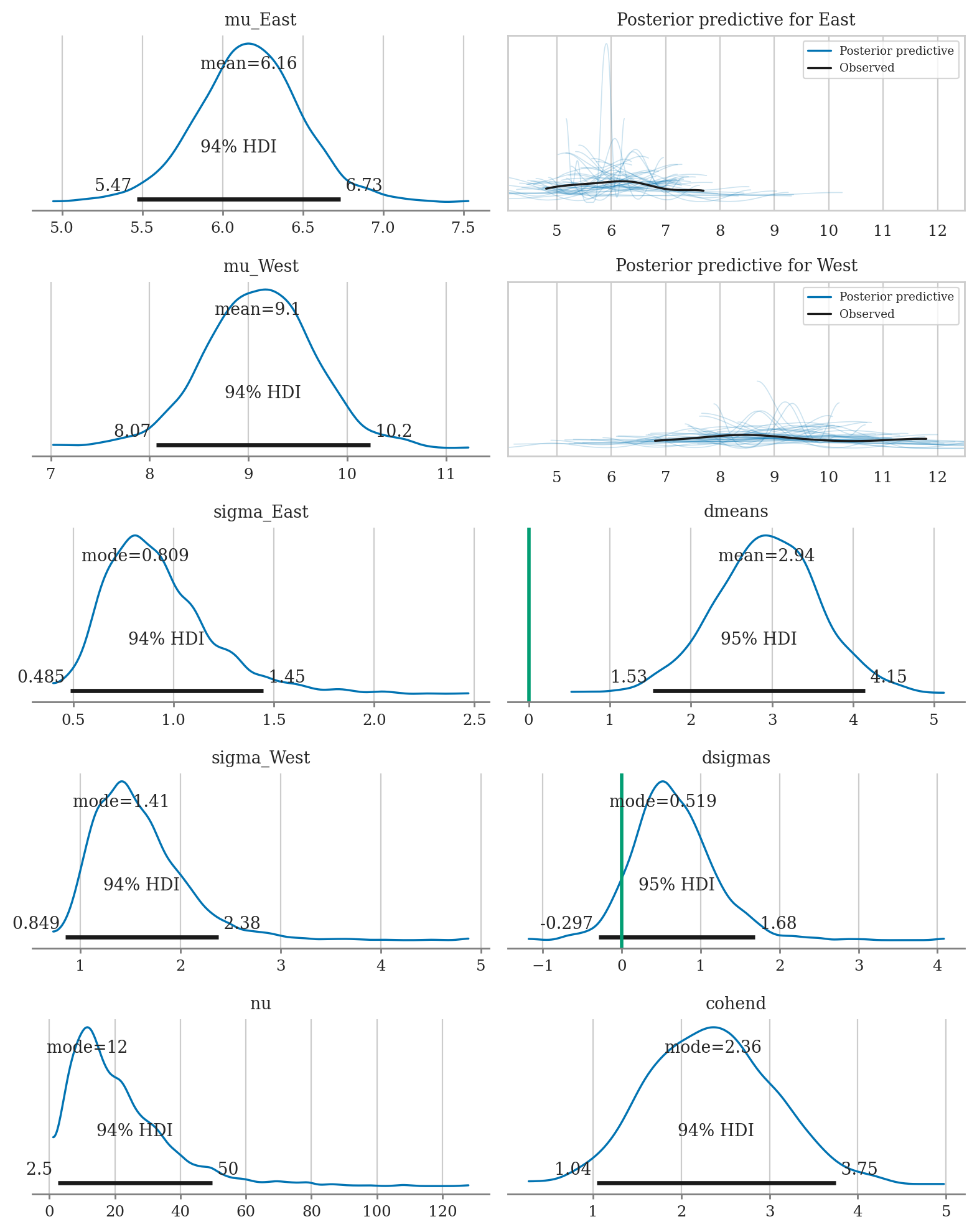

Processing the results#

Calculate derived quantities used for the analysis plots and summaries.

post1 = idata1["posterior"]

# Calculate sigmas from log-sigmas

#######################################################

logsig_W = post1["sigma_loc"].sel(sigma_loc_dim="West")

logsig_E = post1["sigma_loc"].sel(sigma_loc_dim="East")

post1["sigma_West"] = np.exp(logsig_W)

post1["sigma_East"] = np.exp(logsig_E)

# Calculate the difference between between means

post1["mu_West"] = post1["loc"].sel(loc_dim="West")

post1["mu_East"] = post1["loc"].sel(loc_dim="East")

post1["dmeans"] = post1["mu_West"] - post1["mu_East"]

# Calculate the difference between standard deviations

post1["dsigmas"] = post1["sigma_West"]-post1["sigma_East"]

# Effect size

#######################################################

pvar =(post1["sigma_West"]**2+post1["sigma_East"]**2)/2

post1["cohend"] = post1["dmeans"] / np.sqrt(pvar)

# #ALT: use helper function

# from ministats import calc_dmeans_stats

# calc_dmeans_stats(idata1, group_name="loc")

az.summary(idata1, kind="stats", hdi_prob=0.90,

var_names=["mu_West", "mu_East", "dmeans", "sigma_West", "sigma_East", "dsigmas", "nu", "cohend"])

| mean | sd | hdi_5% | hdi_95% | |

|---|---|---|---|---|

| mu_West | 9.099 | 0.571 | 8.221 | 10.041 |

| mu_East | 6.163 | 0.333 | 5.616 | 6.681 |

| dmeans | 2.936 | 0.660 | 1.853 | 4.027 |

| sigma_West | 1.583 | 0.459 | 0.929 | 2.223 |

| sigma_East | 0.927 | 0.276 | 0.546 | 1.342 |

| dsigmas | 0.656 | 0.520 | -0.183 | 1.440 |

| nu | 21.451 | 15.481 | 2.189 | 41.225 |

| cohend | 2.351 | 0.726 | 1.276 | 3.611 |

from ministats import plot_dmeans_stats

plot_dmeans_stats(mod1, idata1, group_name="loc");

Compare to frequentist results#

from scipy.stats import ttest_ind

pricesW = eprices[eprices["loc"]=="West"]["price"]

pricesE = eprices[eprices["loc"]=="East"]["price"]

res1 = ttest_ind(pricesW, pricesE, equal_var=False)

res1.statistic, res1.pvalue

(5.022875513276464, 0.0002570338337217615)

res1.confidence_interval(confidence_level=0.9)

ConfidenceInterval(low=1.9396575883680867, high=4.060342411631915)

from ministats import cohend2

cohend2(pricesW, pricesE)

2.3678062243290996

Conclusions#

Example 2: comparing IQ scores#

We’ll look at IQ scores data taken from a the paper Bayesian Estimation Supersedes the t-Test (BEST) by John K. Kruschke.

smart drug administered to treatment group and want to compare to control group. Data contains outliers)

cf. compare_iqs2_many_ways.ipynb

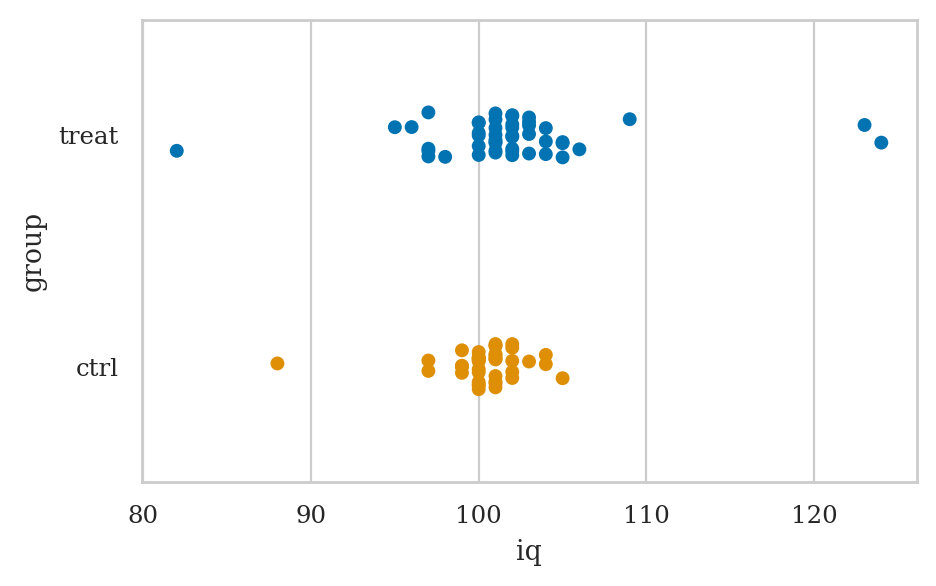

IQ scores dataset#

iqs2 = pd.read_csv("datasets/iqs2.csv")

iqs2.groupby("group")["iq"].describe()

| count | mean | std | min | 25% | 50% | 75% | max | |

|---|---|---|---|---|---|---|---|---|

| group | ||||||||

| ctrl | 42.0 | 100.357143 | 2.516496 | 88.0 | 100.0 | 100.5 | 101.0 | 105.0 |

| treat | 47.0 | 101.914894 | 6.021085 | 82.0 | 100.0 | 102.0 | 103.0 | 124.0 |

sns.stripplot(data=iqs2, x="iq", y="group", hue="group");

Bayesian model#

TODO: add formulas

Bambi model#

formula2 = bmb.Formula("iq ~ 0 + group",

"sigma ~ 0 + group")

priors2 = {

"group": bmb.Prior("Normal", mu=100, sigma=35),

"sigma": {

"group": bmb.Prior("Normal", mu=1, sigma=2)

},

"nu": bmb.Prior("Gamma", alpha=2, beta=0.1),

}

mod2 = bmb.Model(formula=formula2,

family="t",

# link={"mu":"identity", "sigma":"log"}, # Bambi defaults

priors=priors2,

data=iqs2)

mod2

Formula: iq ~ 0 + group

sigma ~ 0 + group

Family: t

Link: mu = identity

sigma = log

Observations: 89

Priors:

target = mu

Common-level effects

group ~ Normal(mu: 100.0, sigma: 35.0)

Auxiliary parameters

nu ~ Gamma(alpha: 2.0, beta: 0.1)

target = sigma

Common-level effects

sigma_group ~ Normal(mu: 1.0, sigma: 2.0)

mod2.build()

mod2.graph()

Model fitting and analysis#

idata2 = mod2.fit(random_seed=42)

Initializing NUTS using jitter+adapt_diag...

Multiprocess sampling (2 chains in 2 jobs)

NUTS: [nu, group, sigma_group]

Sampling 2 chains for 1_000 tune and 1_000 draw iterations (2_000 + 2_000 draws total) took 2 seconds.

We recommend running at least 4 chains for robust computation of convergence diagnostics

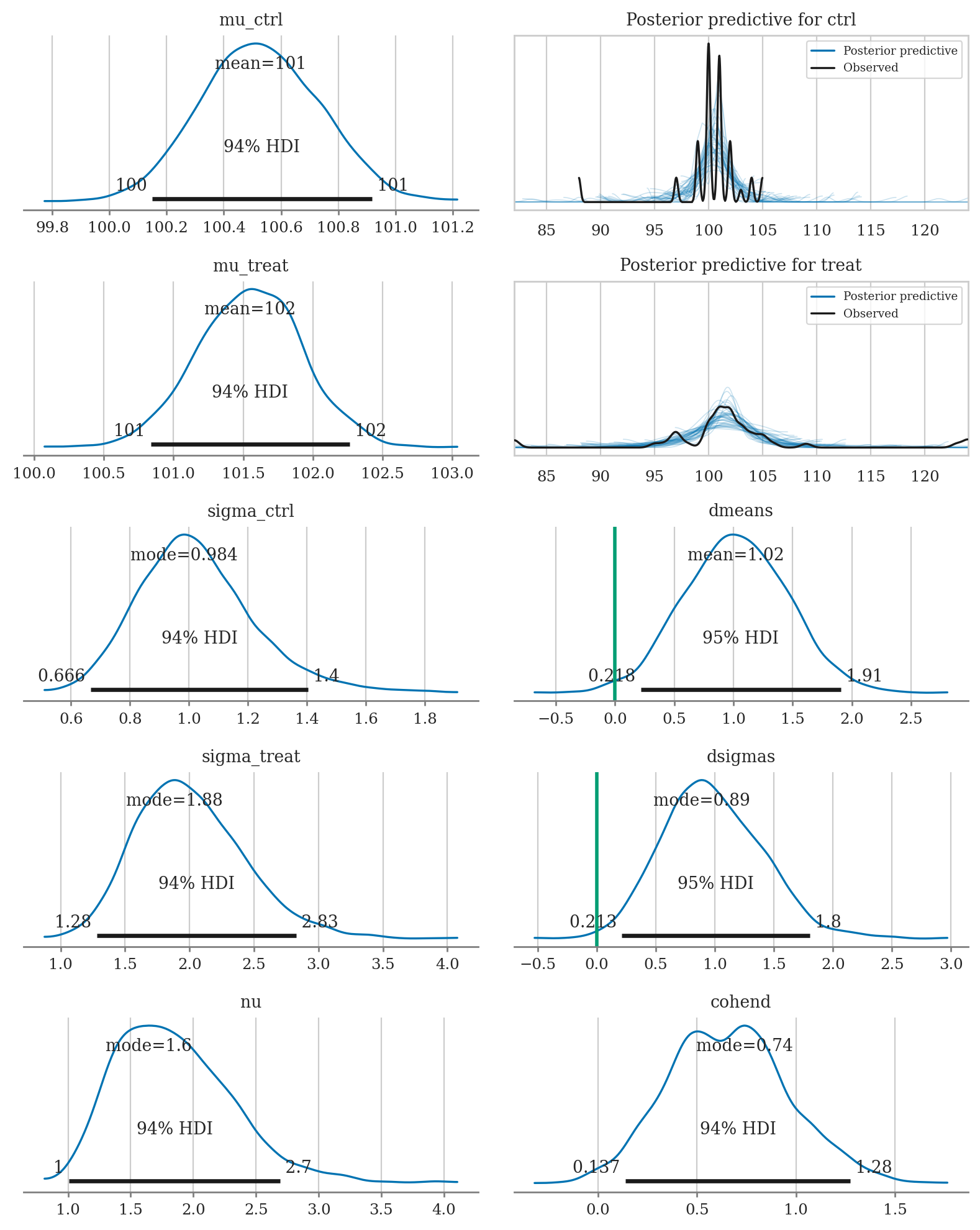

from ministats import calc_dmeans_stats

calc_dmeans_stats(idata2, group_name="group");

az.summary(idata2, kind="stats", hdi_prob=0.95,

var_names=["mu_treat", "mu_ctrl", "dmeans", "sigma_treat", "sigma_ctrl", "dsigmas", "nu", "cohend"])

| mean | sd | hdi_2.5% | hdi_97.5% | |

|---|---|---|---|---|

| mu_treat | 101.547 | 0.379 | 100.807 | 102.285 |

| mu_ctrl | 100.528 | 0.209 | 100.150 | 100.947 |

| dmeans | 1.019 | 0.441 | 0.218 | 1.907 |

| sigma_treat | 2.006 | 0.422 | 1.228 | 2.839 |

| sigma_ctrl | 1.026 | 0.201 | 0.663 | 1.437 |

| dsigmas | 0.980 | 0.426 | 0.213 | 1.803 |

| nu | 1.859 | 0.487 | 1.002 | 2.773 |

| cohend | 0.660 | 0.307 | 0.091 | 1.291 |

from ministats import plot_dmeans_stats

plot_dmeans_stats(mod2, idata2, group_name="group", ppc_xlims=[82,124]);

Sensitivity analysis#

from ministats.book.tables import sens_analysis_dmeans_iqs2

results = sens_analysis_dmeans_iqs2(iqs2)

results

| M_prior | logSigma_prior | Nu_prior | dmeans_mean | dmeans_95hdi | dsigmas_mode | dsigmas_95hdi | nu_mode | codhend_mode | |

|---|---|---|---|---|---|---|---|---|---|

| 0 | $\mathcal{N}(100,35)$ | $\mathcal{N}(1,2)$ | $\Gamma(2,0.1)$ | 1.02 | [0.232, 1.907] | 0.897 | [0.213, 1.858] | 1.672 | 0.897 |

| 1 | $\mathcal{N}(100,50)$ | $\mathcal{N}(1,2)$ | $\Gamma(2,0.1)$ | 1.014 | [0.207, 1.888] | 0.932 | [0.143, 1.823] | 1.71 | 0.932 |

| 2 | $\mathcal{N}(100,10)$ | $\mathcal{N}(1,2)$ | $\Gamma(2,0.1)$ | 1.026 | [0.227, 1.917] | 0.905 | [0.201, 1.829] | 1.724 | 0.905 |

| 3 | $\mathcal{N}(100,35)$ | $\mathcal{N}(0,1)$ | $\Gamma(2,0.1)$ | 1.027 | [0.193, 1.838] | 0.831 | [0.178, 1.714] | 1.608 | 0.831 |

| 4 | $\mathcal{N}(100,35)$ | $\mathcal{N}(1,2)$ | $\textrm{Expon}(1/30)$ | 1.027 | [0.261, 1.867] | 0.795 | [0.217, 1.882] | 1.6 | 0.795 |

Compare to frequentist results#

from scipy.stats import ttest_ind

treated = iqs2[iqs2["group"]=="treat"]["iq"]

controls = iqs2[iqs2["group"]=="ctrl"]["iq"]

res2 = ttest_ind(treated, controls, equal_var=False)

res2.statistic, res2.pvalue

(1.622190457290228, 0.10975381983712833)

res2.confidence_interval(confidence_level=0.95)

ConfidenceInterval(low=-0.3611847723663688, high=3.476686292123202)

from ministats import cohend2

cohend2(treated, controls)

0.33096545301397307

# MAYBE

# # Test if the variances of the two groups are the same

# from scipy.stats import levene

# levene(treated, controls)

Conclusions#

Explanations#

Alternative choices of priors#

e.g. prior for sigma as very wiiiiiide, and nu ~ Exp(1/29)+1 → BEST Bayesian estimation supersedes the t-test by John K. Kruschke

If we use a model with common standard deviation, we get equivalent of pooled sigma

# TODO

Performance tests#

Simulated datasets#

Simulate datasets with various combinations of \(n\), \(\Delta\), and outliers.

from ministats.book.tables import gen_dmeans_datasets

ns = [20, 30, 50, 100]

Deltas = [0, 0.2, 0.5, 0.8, 1.3]

outliers_options = ["no", "few", "lots"]

dataset_specs = gen_dmeans_datasets(ns=ns,

Deltas=Deltas,

outliers_options=outliers_options)

dataset_specs[0:4]

[{'n': 20, 'Delta': 0, 'outliers': 'no', 'random_seed': 45},

{'n': 20, 'Delta': 0, 'outliers': 'few', 'random_seed': 46},

{'n': 20, 'Delta': 0, 'outliers': 'lots', 'random_seed': 47},

{'n': 20, 'Delta': 0.2, 'outliers': 'no', 'random_seed': 48}]

Model comparisons#

Compare results several models:

Classical permutation test (from Section 4.5)

Classical Welch’s two-sample t-test (from Section 4.5)

Bayesian model with \(\mathcal{N}\) data model

Robust Bayesian model with \(\mathcal{T}\) data model

Bayes factors with JZS prior and standard cutoff

from ministats.book.tables import fit_dmeans_models

help(fit_dmeans_models)

Help on function fit_dmeans_models in module ministats.book.tables:

fit_dmeans_models(dataset, random_seed=42)

Fit the following models for the difference of two means:

- Permutation test from Section 3.5

- Welch's two-sample $t$-test from Section 3.5

- Bayesian model that uses normal as data model

- Robust Bayesian model that uses t-distribution as data model

- Bayes factor using JZS prior (using `pingouin` library)

For each model, we run the hypothesis test to decide if the populations

are the same or different based on the conventional cutoff level of 5%.

We also construct a 90% interval estimates for the unknown `Delta`.

Results#

# Download simdata/ directory if necessary

from ministats import ensure_simdata

ensure_simdata()

# Option A: load results from simulation

filename = "dmeans_perf_metrics__" \

+ "ns_20_30_50_100__" \

+ "Deltas_0_0.2_0.5_0.8_1.3__" \

+ "outs_no_few_lots__reps_100.csv"

results = pd.read_csv(os.path.join("simdata", filename), index_col=[0,1])

results.head(3)

# Option B: run full simulation (takes about three days)

# from ministats.book.tables import calc_dmeans_perf_metrics

# results = calc_dmeans_perf_metrics(reps=100)

simdata/ directory present and ready.

| n | Delta | outliers | seed | count_reject | count_fail_to_reject | count_captured | avg_width | ||

|---|---|---|---|---|---|---|---|---|---|

| spec | model | ||||||||

| 0 | perm | 20 | 0.0 | no | 45 | 6 | 94 | 90.0 | 1.011714 |

| welch | 20 | 0.0 | no | 45 | 6 | 94 | 90.0 | 1.065525 | |

| norm_bayes | 20 | 0.0 | no | 45 | 2 | 98 | 94.0 | 1.294730 |

Type I (false positive) error rates#

from ministats.book.tables import get_perf_table_typeI

tableA = get_perf_table_typeI(results)

tableA

| model | perm | welch | norm_bayes | robust_bayes | bf | |

|---|---|---|---|---|---|---|

| outliers | n | |||||

| no | 20 | 0.06 | 0.06 | 0.02 | 0.07 | 0.02 |

| 30 | 0.04 | 0.04 | 0.03 | 0.04 | 0.03 | |

| 50 | 0.04 | 0.04 | 0.01 | 0.04 | 0.01 | |

| 100 | 0.06 | 0.06 | 0.03 | 0.05 | 0.01 | |

| few | 20 | 0.04 | 0.04 | 0.01 | 0.05 | 0.01 |

| 30 | 0.04 | 0.04 | 0.01 | 0.05 | 0.00 | |

| 50 | 0.03 | 0.03 | 0.02 | 0.01 | 0.00 | |

| 100 | 0.07 | 0.07 | 0.06 | 0.08 | 0.03 | |

| lots | 20 | 0.04 | 0.02 | 0.01 | 0.03 | 0.01 |

| 30 | 0.02 | 0.02 | 0.00 | 0.02 | 0.00 | |

| 50 | 0.07 | 0.06 | 0.06 | 0.07 | 0.04 | |

| 100 | 0.03 | 0.03 | 0.03 | 0.02 | 0.00 |

Observations:

all models are about the same

BF model has significantly less false positives

Power analysis#

from ministats.book.tables import get_perf_table_power

tableB = get_perf_table_power(results, show_all=False)

tableB

| model | perm | welch | norm_bayes | robust_bayes | bf | ||

|---|---|---|---|---|---|---|---|

| outliers | Delta | n | |||||

| no | 0.5 | 30 | 0.46 | 0.46 | 0.33 | 0.46 | 0.31 |

| 50 | 0.68 | 0.69 | 0.54 | 0.66 | 0.50 | ||

| 100 | 0.93 | 0.93 | 0.90 | 0.93 | 0.84 | ||

| 0.8 | 20 | 0.60 | 0.60 | 0.44 | 0.59 | 0.49 | |

| 30 | 0.86 | 0.86 | 0.77 | 0.86 | 0.72 | ||

| 50 | 0.99 | 0.99 | 0.96 | 0.99 | 0.93 | ||

| few | 0.5 | 30 | 0.49 | 0.49 | 0.32 | 0.45 | 0.29 |

| 50 | 0.49 | 0.51 | 0.39 | 0.58 | 0.33 | ||

| 100 | 0.80 | 0.80 | 0.80 | 0.88 | 0.69 | ||

| 0.8 | 20 | 0.69 | 0.68 | 0.51 | 0.65 | 0.54 | |

| 30 | 0.88 | 0.88 | 0.79 | 0.87 | 0.78 | ||

| 50 | 0.85 | 0.85 | 0.83 | 0.94 | 0.75 | ||

| lots | 0.5 | 30 | 0.33 | 0.32 | 0.29 | 0.43 | 0.20 |

| 50 | 0.52 | 0.52 | 0.50 | 0.63 | 0.33 | ||

| 100 | 0.64 | 0.63 | 0.60 | 0.88 | 0.52 | ||

| 0.8 | 20 | 0.44 | 0.43 | 0.37 | 0.63 | 0.30 | |

| 30 | 0.60 | 0.59 | 0.57 | 0.81 | 0.48 | ||

| 50 | 0.82 | 0.83 | 0.79 | 0.97 | 0.66 |

Observations:

Bayes \(\mathcal{T}\) has higher power than Bayes \(\mathcal{N}\)

Bayes \(\mathcal{T}\) outperforms all other models when outliers are present

Interval estimates coverage#

from ministats.book.tables import get_perf_table_coverage

tableC = get_perf_table_coverage(results)

tableC

| model | perm | welch | norm_bayes | robust_bayes | |||||

|---|---|---|---|---|---|---|---|---|---|

| coverage | avg_width | coverage | avg_width | coverage | avg_width | coverage | avg_width | ||

| outliers | n | ||||||||

| no | 20 | 0.8800 | 1.011711 | 0.9050 | 1.064862 | 0.9650 | 1.298070 | 0.9100 | 1.078473 |

| 30 | 0.9100 | 0.821001 | 0.9175 | 0.849298 | 0.9625 | 1.016220 | 0.9225 | 0.855460 | |

| 50 | 0.9050 | 0.651732 | 0.9100 | 0.665610 | 0.9525 | 0.762513 | 0.9100 | 0.667750 | |

| 100 | 0.9025 | 0.462228 | 0.9025 | 0.467091 | 0.9325 | 0.517568 | 0.9075 | 0.467747 | |

| few | 20 | 0.8550 | 1.002797 | 0.8675 | 1.056252 | 0.9500 | 1.294572 | 0.8700 | 1.069132 |

| 30 | 0.9175 | 0.835295 | 0.9250 | 0.864310 | 0.9625 | 1.022407 | 0.9250 | 0.872108 | |

| 50 | 0.8675 | 0.784709 | 0.9025 | 0.802027 | 0.9350 | 0.854340 | 0.9075 | 0.695260 | |

| 100 | 0.8725 | 0.554332 | 0.8975 | 0.560776 | 0.9125 | 0.581300 | 0.9275 | 0.487010 | |

| lots | 20 | 0.8700 | 1.442238 | 0.9025 | 1.530370 | 0.9450 | 1.601472 | 0.8975 | 1.197020 |

| 30 | 0.8550 | 1.085291 | 0.8700 | 1.128444 | 0.9000 | 1.197037 | 0.8550 | 0.926892 | |

| 50 | 0.8825 | 0.892523 | 0.8975 | 0.913113 | 0.9175 | 0.937645 | 0.9075 | 0.726270 | |

| 100 | 0.8975 | 0.679404 | 0.9025 | 0.686951 | 0.9175 | 0.688840 | 0.8950 | 0.509295 | |

Observations:

All methods have coverage close to the nominal 90%

Bayes \(\mathcal{T}\) produces narrower intervals

Discussion#

Comparison to the frequentist two-sample t-test#

results numerically similar

note we’re using 𝒯 as data model, not as a sampling distribution

conceptually different:

p-value vs. decision based on posterior distribution

confidence intervals vs. credible intervals

Comparing multiple groups#

?Extension to Bayesian ANOVA? Can extend approach to multiple groups: Bayesian ANOVA

FWD reference to hierarchical models for group comparison covered in Section 5.5

Exercises#

Exercise 1: small samples#

As = [5.77, 5.33, 4.59, 4.33, 3.66, 4.48]

Bs = [3.88, 3.55, 3.29, 2.59, 2.33, 3.59]

groups = ["A"]*len(As) + ["B"]*len(Bs)

df1 = pd.DataFrame({"group": groups, "vals": As + Bs})

# df1

Exercise 2: lecture and debate curriculums#

students = pd.read_csv("datasets/students.csv")

# students.groupby("curriculum")["score"].describe()

formula_std = bmb.Formula("score ~ 0 + curriculum",

"sigma ~ 0 + curriculum")

priors_std = {

"curriculum": bmb.Prior("Normal", mu=70, sigma=30),

"sigma": {

"curriculum":bmb.Prior("Normal", mu=1, sigma=2)

},

"nu": bmb.Prior("Gamma", alpha=2, beta=0.1),

}

mod_std = bmb.Model(formula=formula_std,

family="t",

link="identity",

priors=priors_std,

data=students)

mod_std

# mod_std.build()

# mod_std.graph()

Formula: score ~ 0 + curriculum

sigma ~ 0 + curriculum

Family: t

Link: mu = identity

sigma = log

Observations: 15

Priors:

target = mu

Common-level effects

curriculum ~ Normal(mu: 70.0, sigma: 30.0)

Auxiliary parameters

nu ~ Gamma(alpha: 2.0, beta: 0.1)

target = sigma

Common-level effects

sigma_curriculum ~ Normal(mu: 1.0, sigma: 2.0)

idata_std = mod_std.fit(random_seed=42)

Initializing NUTS using jitter+adapt_diag...

Multiprocess sampling (2 chains in 2 jobs)

NUTS: [nu, curriculum, sigma_curriculum]

Sampling 2 chains for 1_000 tune and 1_000 draw iterations (2_000 + 2_000 draws total) took 2 seconds.

We recommend running at least 4 chains for robust computation of convergence diagnostics

# Calculate the difference between between means

currs = idata_std["posterior"]["curriculum"]

mu_debate = currs.sel(curriculum_dim="debate")

mu_lecture = currs.sel(curriculum_dim="lecture")

idata_std["posterior"]["dmeans"] = mu_debate - mu_lecture

az.summary(idata_std, kind="stats", var_names=["dmeans"], hdi_prob=0.95)

| mean | sd | hdi_2.5% | hdi_97.5% | |

|---|---|---|---|---|

| dmeans | 7.685 | 5.428 | -3.012 | 18.201 |

# from ministats import plot_dmeans_stats

# plot_dmeans_stats(mod_std, idata_std, ppc_xlims=[50,100], group_name="curriculum");

# from scipy.stats import ttest_ind

# scoresD = students[students["curriculum"]=="debate"]["score"]

# scoresL = students[students["curriculum"]=="lecture"]["score"]

# res_std = ttest_ind(scoresD, scoresL, equal_var=False)

# res_std.statistic, res_std.pvalue

# from ministats import cohend2

# cohend2(scoresL, scoresD)

Exercise 3: redo exercises from Section 3.5 section using Bayesian methods#

# TODO

Links#

TODO

BONUS Examples#

Example 4: small example form BEST vignette#

See http://cran.nexr.com/web/packages/BEST/vignettes/BEST.pdf#page=2

# y1s = [5.77, 5.33, 4.59, 4.33, 3.66, 4.48]

# y2s = [3.88, 3.55, 3.29, 2.59, 2.33, 3.59]

# from ministats.bayes import bayes_dmeans

# mod4, idata4 = bayes_dmeans(y1s, y2s, groups=["y1", "y2"])

# from ministats import calc_dmeans_stats

# calc_dmeans_stats(idata4)

# az.summary(idata4, kind="stats", hdi_prob=0.95,

# var_names=["dmeans", "sigma_y1", "sigma_y2", "dsigmas", "nu", "cohend"])

# from ministats import plot_dmeans_stats

# plot_dmeans_stats(mod4, idata4, ppc_xlims=None);

Example 5: comparing morning to evening#

# morning = [8.99, 9.21, 9.03, 9.15, 8.68, 8.82, 8.66, 8.82, 8.59, 8.14,

# 9.09, 8.80, 8.18, 9.23, 8.55, 9.03, 9.36, 9.06, 9.57, 8.38]

# evening = [9.82, 9.34, 9.73, 9.93, 9.33, 9.41, 9.48, 9.14, 8.62, 8.60,

# 9.60, 9.41, 8.43, 9.77, 8.96, 9.81, 9.75, 9.50, 9.90, 9.13]

# from ministats.bayes import bayes_dmeans

# mod5, idata5 = bayes_dmeans(evening, morning, groups=["evening", "morning"])

# from ministats import calc_dmeans_stats

# calc_dmeans_stats(idata5)

# az.summary(idata5, kind="stats", hdi_prob=0.95,

# var_names=["dmeans", "sigma_evening", "sigma_morning", "dsigmas", "nu", "cohend"])

# from ministats import plot_dmeans_stats

# plot_dmeans_stats(mod5, idata5, ppc_xlims=None);